Politics

How Buy-Now-Pay-Later is Changing the E-Commerce Landscape

The e-commerce landscape is constantly evolving. With more ways to access the world of online shopping than ever before, consumers continue to seek new and innovative ways to purchase their favourite products.

Buy now, pay later (BNPL) has begun to revolutionise the e-commerce industry. After being rapidly adopted as the globe’s newest preferred method of payment, BNPL platforms like Klarna and Paypal have become the go-to apps for a fuss-free omnichannel shopping experience.

In fact, a whopping 70% of buy now, pay later users claim that they would no longer opt to purchase from e-commerce stores without flexible and convenient payment options. Not only does this give brands with BNPL in place a competitive edge, but it means that smaller stores can no longer sleep on flexible financing.

The BNPL market is tipped to be worth more than $3 trillion in 2030. As the e-commerce industry prepares for another digital shift, here’s why you need to be ahead of this new financial curve.

What is Buy Now, Pay Later?

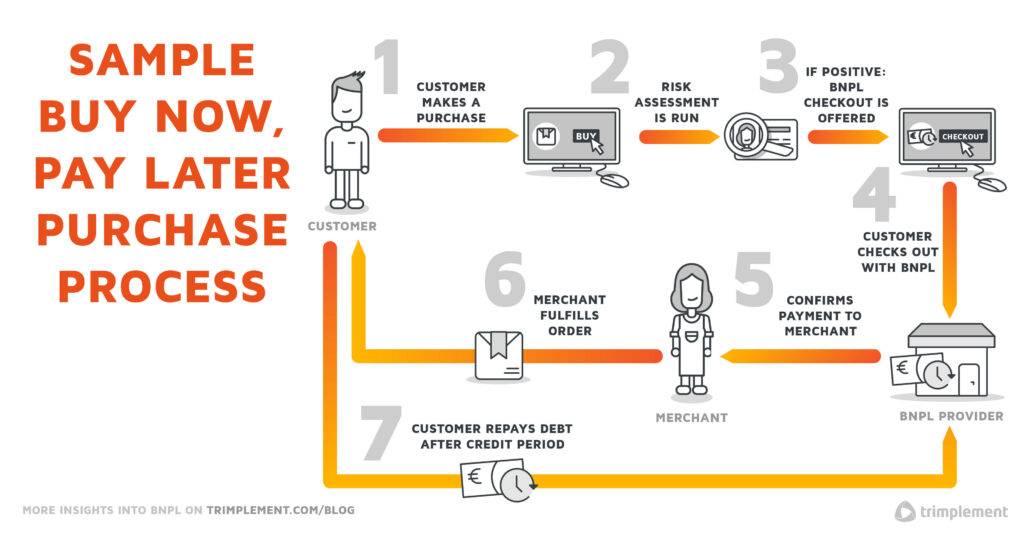

Buy now, pay later is one of the newest payment options revolutionising the e-commerce conversion process. BNPL works by splitting a customer’s payment across a number of weeks or months, depending on the payment plan they choose.

The first payment is then taken directly at checkout before the rest of the payments are taken out in further instalments.

“The payments landscape is ever-evolving. BNPL has proven to be a trusted payment method for consumers, and the demand for flexible and simple payment choices grows as additional fintechs and large corporations join the BNPL space,” says Bryce Deeney, cofounder and CEO of Equipifi. The time is now for financial institutions to determine where BNPL fits within their core product offerings and their strategic initiatives.”

(Image Source: Trimplement)

In terms of consumers, BNPL offers a wide range of benefits ranging from lower checkout fees, little to no interest rates and flexibility that no other payment service can provide. In fact, over 37% of consumers believe that BNPL is the most convenient way to pay for their online shopping.

The question is, how is it transforming the success of e-commerce retailers?

Can Retailers Use BNPL to Their Advantage?

Adding a more convenient payment system into the mix has increased e-commerce conversions tenfold. In an era of high inflation rates and more abandoned shopping carts than ever before, introducing a BNPL system to your checkout could play a key role in keeping your e-commerce store alive and kicking.

“BNPL isn’t going anywhere, but your cardholders may be. As the new year approaches and your institution evaluates your tech stack, make sure BNPL is part of the equation,” says Deeney. “Look into partners that allow for BNPL while also working seamlessly with your current technology and payment processing solutions. This will help make the transition easier for everyone involved.”

If you’re still unsure about the potential benefits of buy now, pay later, here’s how you could use flexible finance to your advantage.

Boosting Conversion Rates

Did you know that BNPL systems can boost store conversion rates by 20-30%? With the ability to split payments into several instalments, e-commerce stores with a buy now pay later scheme find that they have fewer abandoned shopping carts and a higher chance of converting leads.

If you’re aiming to increase your conversion rate, it might be time to introduce BNPL to your conversion funnel. Depending on your target audience and how likely they would be to engage with a split payment system, BNPL could grant you a competitive advantage.

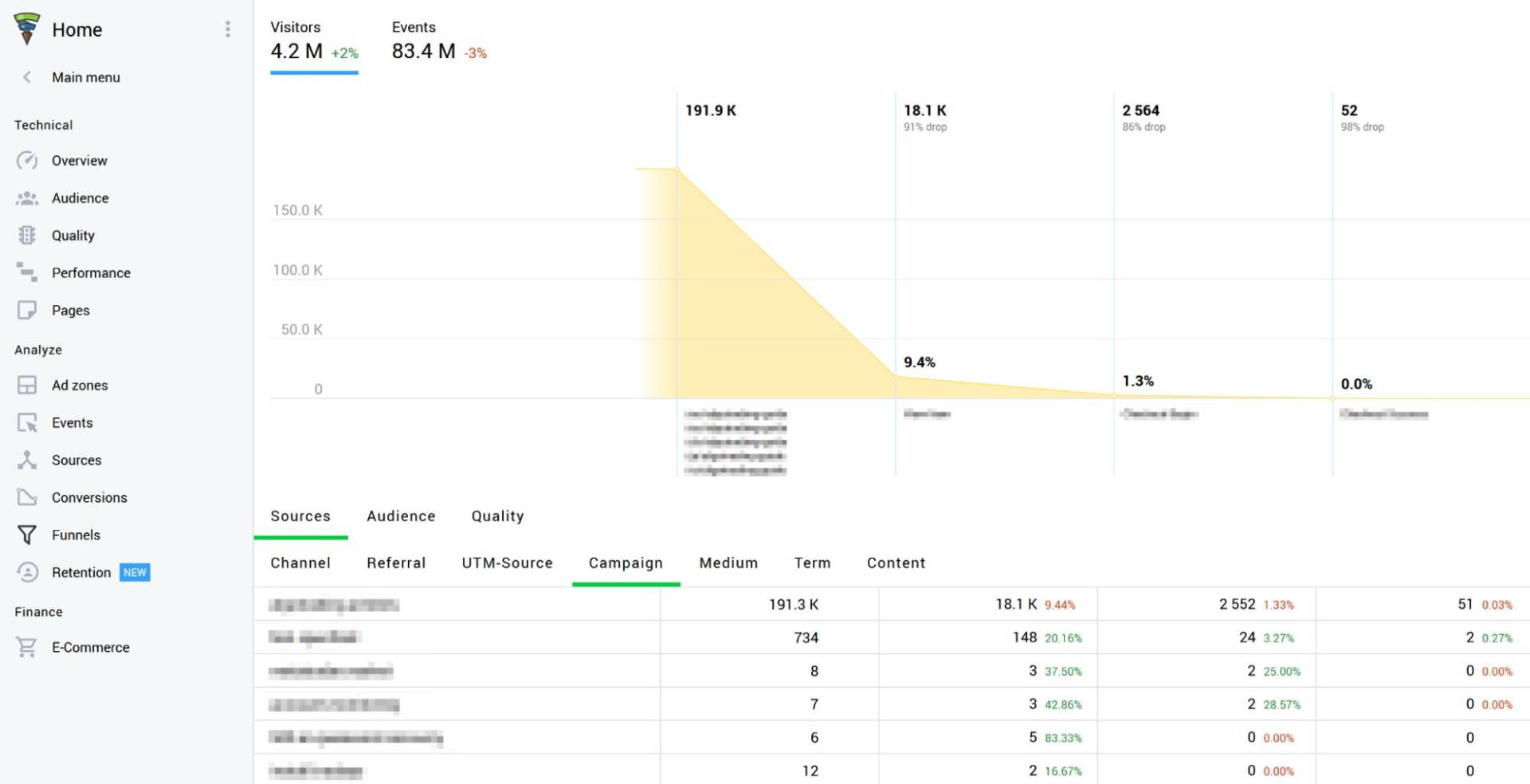

The key here is to start researching your target demographic. Using an analytic tool such as Finteza, you can quickly learn more about your audience’s behaviour and identify the exact points where they drop off of the funnel. Below is the example of a funnel used to attract visitors to sign up for an affiliate program.

For example, if your largest site weak point is the checkout, it could suggest that the payment process is either tricky to access, slow loading or unaffordable. Adding a new payment option, like BNPL, into the mix could encourage a more inclusive future and influence leads to make that all-important purchase.

Using Finteza, you can quickly access audience data and segment your traffic sources into 15 basic parameters, including location, events, page addresses and even the type of device a visitor accesses from.

Gaining a wider insight into how your target consumers function could suggest whether they are likely to utilise a BNPL payment plan. With the average BNPL user aged 18-35, e-commerce stores with a much older demographic may end up shying away from a pay-later scheme.

(Image Source: Exploding Topics)

Finteza can also be used to further optimise your sales and conversion funnel before introducing a BNPL system. With the ability to spot weak points in a sales system, Finteza can draw up real-time reports in seconds, revealing where visitors are most likely to leave a site or which pages are the most susceptible to bouncing.

If you’re aiming to trial a BNPL scheme, why not test your success using an AI-generated analytic partner? Finteza, for example, can even track the number of times a mouse hovers over certain page points, which could aid you in identifying just how many consumers are interested in flexible finance.

Improving Customer Experience

Did you know that 41% of the younger generation now say that they would rather use BNPL services for all household purchases?

Buy now, pay later systems allow for a more inclusive shopping experience. Not only do platforms like Klarna and Split It pride themselves on providing financial flexibility, but they have also become the most affordable form of payment for those suffering the consequences of inflation and a cost-of-living crisis.

Introducing inclusive payment methods to your e-commerce store opens it up to more potential customers. Especially if your target audience is within a younger generation, Adding Klaran options at the checkout will ensure that your store remains in line with current high-street shopping trends alongside popular online retail platforms such as TikTok shop and ASOS.

A New Competitive Edge

According to experts at Baymard, 70% of carts are now abandoned by modern-day consumers due to a lack of preferred payment options. Implementing a buy now, pay later option could help your store solve this challenge for your target leads and become the online store they pick in a sea full of competitors.

While Klarna, PayPal and other flexible finance apps continue to dominate the BNPL landscape, it seems as if other e-commerce giants aren’t far behind with their own versions of ‘split-pay’. Amazon introduced their own buy now, pay later scheme in early 2022 for orders over £100. With other tech giants such as Apple not far behind, could flexible finance pioneer the future of online commerce?

BNPL transactions are set to exceed $680 billion by 2025, making it one of the most used payment choices across the globe in the last decade. Allowing more shoppers to complete a purchase could result in higher order values and increased conversion rates. The question is, will you step aboard the BNPL ship or simply embrace the wave?